The cryptocurrency market has been under a period of duress, with a majority of the tokens in the cryptoverse witnessing a price slump that has set in since the first week of December. The flagship cryptocurrency token, Bitcoin (BTC), underwent a flash crash on Dec. 4, wherein the price of the token fell below $50,000 in nearly two months, as per data from Cointelegraph Markets Pro.

This phenomenon was witnessed among the majority of the cryptocurrency tokens as the market was gradually painted in red. Ethereum and Ether (ETH) came to be the network and token of choice for a majority of decentralized finance (DeFi) protocols as Ether witnessed a 19% price drop.

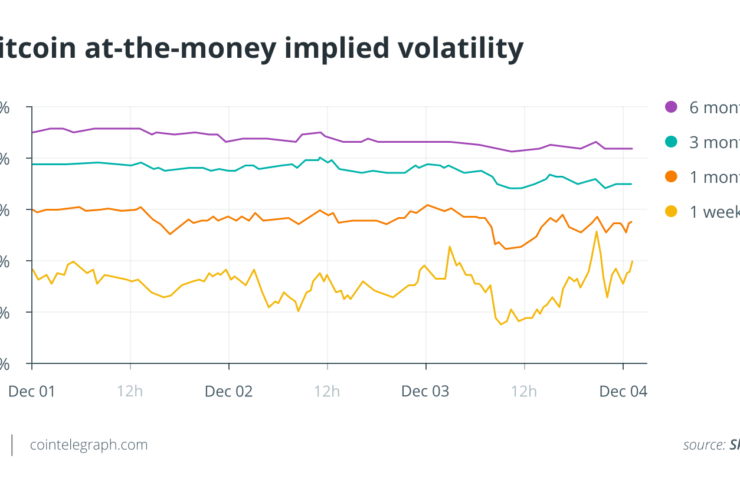

However, BTC and ETH also have a healthy futures and options market that could’ve played an important role in foreseeing this ongoing price slump for these tokens.

Coinindicing with the price crash on Dec. 4, $950 million worth of BTC options expired, wherein bears had the advantage over the bulls even at the time when the price was trading at $57,000. The options data leading up to this expiry suggested that it was skewed toward the market forces being bearish due to a high proportion of put options below the $57,000 mark. A put option is a contract that gives the holder of the option the right (but not the obligation) to sell a predefined amount of the underlying asset at a predetermined price.

A call option is one in which the option holder has the right to buy the underlying assets under similar conditions. The proportion of put options in comparison with the call options leading up to an options expiry is highly indicative of the sentiment that prevails in the market for the underlying asset. In this case, there was a clear indication that markets were heavily bearish even a week before the expiry and the price flash that went hand in hand.

The forces in play

Luuk Strijers, the chief commercial officer of crypto derivatives exchange Deribit, spoke to Cointelegraph about the signs in the derivatives data that gave an inkling about the incoming crash:

“Prior to the weekend correction, we saw a spike in IVs possibly related to post-expiry related selling. There seemed to be some uncertainty in the market, and we saw Risk-reversal strategies being traded (Sell OTM Call + Buy OTM Put).”

Since the expiration date for an option is the last date on which the option holder can either decide to exercise the option of either executing the buy or sell order of the underlying asset or the holder deciding to forfeit the option and let it expire becoming worthless, expiries often become significant events that impact the price dynamics of the underlying asset, in this case, Bitcoin.

Strijers opined on the impact of this particular expiry on BTC, saying: “Difficult to tell for certain. However, more and more people watch the expiry and open interest levels at certain key strikes which amplifies the relevance of the larger expiries.”

Adam James, senior analyst at OKEx Insights, the research arm of crypto exchange OKEx, spoke with Cointelegraph about signs leading up to this crash: “The most obvious signs that a crash may be impending were the extremely high open interest and positive funding. Those two things don’t generally bode well and often require a flush.” He added further:

“The cascading sell-off we saw on Saturday was just that flush — thin weekend order books made it easy to steamroll overleveraged longs and cause something of an OI reset. As it happened, the crash was one of the largest capitulating events in BTC’s history.”

Despite this phenomenon being an indication that the price of the underlying assets and the derivatives markets are closely related, the size of the markets is still only a blip on the size of the spot markets.

Institutional investors could be the game-changer

Considering the derivatives markets that exist for the top two cryptocurrency tokens, BTC and ETH — though with significant growth in open interest — it is a very small percentage of the spot markets and its current market capitalization for their assets.

The open interest (OI) for BTC options has grown more than tenfold from nearly $1 billion on July 1 to stand at around $11.4 billion at the time of writing. The OI hit an all-time high of $15.72 billion on Oct. 20. Soon after, BTC hit an all-time high of $68,789.63 on Nov. 10.

Considering that the total market capitalization of BTC in the spot markets in the same duration was over $1 trillion, it is highly evident that cryptocurrency options are only in their nascent stages and, even still, play a vital role in the price discovery and forecasting abilities for the asset. A similar phenomenon is observed when taking a closer look at the OI data for ETH too.

Cointelegraph discussed the size of the crypto options markets with Igneus Terrenus, head of communications at cryptocurrency derivatives exchange Bybit: “When you compare it either to the options market in the commodities space or what Robinhood offers for stocks, what is currently available in the crypto options market seems to be inadequate for both institutional and retail traders.”

Institutional investors could be the game-changer to enable drastic change in the crypto derivatives market by exponentially increasing the size, liquidity and depth of these markets. Goldman Sachs, the investment banking giant that revived its defunct cryptocurrency trading desk amid this bull run, predicted that the cryptocurrency options market could be seen as the next frontier for institutional adoption of crypto. The wall street bank themselves announced plans to expand their crypto trading desk to engage with BTC and ETH derivatives products as well.

However, Strijers explained that institutional investors coming into the crypto derivatives market is a slow-moving process, especially due to Know Your Customer (KYC) and due diligence processes. He said, “In November, we have onboarded more institutional clients than any month before — the larger the firm, the longer the mutual onboarding process.” He went on to add:

“Now, those large clients have an extensive platform and a due diligence procedure as well, especially the ones offering third party asset management in some form, like the multi-billion dollar macro funds, for example.”

Other Altcoins play catch up

Currently, there is a liquid options market that exists only for BTC and ETH on various cryptocurrency exchanges like Deribit, LedgerX, OKEx, FTX and even the Chicago Mercantile Exchange (CME), the largest derivatives exchange in the world for traditional asset classes.

However, there are no options products available for other prominent cryptocurrency tokens like XRP (XRP), Solana (SOL), Binance Coin (BNB), Polkadot (DOT), and many others, even though these tokens have a highly liquid spot market and even a futures market.

Strijers explained further the reasoning behind this existing scenario: “We plan to make SOL products available soon. Beyond that, it remains to be seen as we require proper market maker coverage at all times, including, for example, Sunday evening and other times, in all strikes and expiries. We can’t rely on a handful of market makers, but need many more.”

Related: Cryptocurrency derivatives market shows growth despite regulatory FUD

Nonetheless, there is also a liquid futures market that is available for several of the top cryptocurrencies, even including the meme coin Dogecoin (DOGE) and the native token of the nonfungible token (NFT) game Axie Infinity (AXS). Even still, the OI of the futures-based products of these tokens hasn’t even touched $1 billion despite the market concluding one of the longest bull runs that the ecosystem has ever witnessed.

The token, apart from BTC and ETH, that has the highest OI for its futures is SOL, standing at nearly $870 million at the time of writing. Next in the ranks is DOT, with an OI of $573 million, followed by BNB with an OI of $521 million.

Considering that all of these altcoins have a spot market capitalization of over $50 billion, the futures market for these tokens is currently only a small proportion of their total market capitalization. This indicates that even though there is a liquid futures market for these assets, its size is very small to have a significant impact on price, although they do play a role in price discovery of the underlying token.

As institutional and retail adoption of cryptocurrencies is seen to be growing by leaps and bounds in the past year, their involvement on the derivatives side of the market will also increase over time, especially once institutional giants like Grayscale jump to the fore and get heavily involved in this market pushing market and pricing efficiencies for these assets.

Comments (No)