Crypto mortgages entail utilizing cryptocurrency holdings as security to bind a conventional mortgage or loan.

The procedure to obtain a crypto-backed mortgage starts with the borrower giving their cryptocurrency to the lender as security, with the lender calculating the maximum loan amount depending on the value of the collateral.

The acceptability of the cryptocurrency is assessed before interest rates, payback terms and term length are decided. The borrower deposits the agreed cryptocurrency sum into the lender’s escrow account once the terms are agreed. In the escrow account, a third party keeps and manages funds, property or documents on behalf of both parties to a transaction until certain criteria are satisfied.

This collateral is kept locked up for the duration of the loan, and to control volatility risks, borrowers frequently need to have a specific buffer between the value of the collateral and the loan balance.

Payments are typically made in fiat money. After repayment is complete, the borrower receives the collateral back. However, a margin call (demand for additional collateral due to fluctuation in collateral value) might happen if the value of the cryptocurrency falls dramatically, in which case the borrower would have to restore the necessary margin.

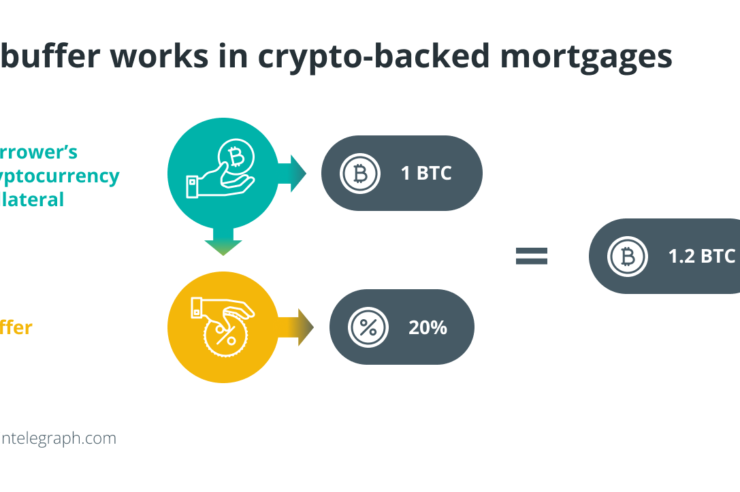

When referring to loans with cryptocurrency as collateral, a buffer is a predetermined percentage difference between the loan balance and the collateral value (cryptocurrency). For instance, if a borrower’s cryptocurrency collateral is valued at 1 BTC and the lender stipulates a 20% buffer, the borrower needs to provide the collateral equivalent to 1.2 BTC (1 BTC 20% of 1 BTC), effectively creating a buffer against potential volatility risks throughout the loan tenure.

This buffer serves as a safety cushion for both the borrower and the lender by preventing changes in the value of the cryptocurrency from instantly resulting in margin calls or the liquidation of collateral.

Comments (No)