This is an opinion editorial by Kudzai Kutukwa, a passionate financial inclusion advocate who was recognized by Fast Company magazine as one of South Africa’s top-20 young entrepreneurs under 30.

The United Fruit Company (AKA El Pulpo which means “the octopus”) was an American company that had an overarching presence in Latin American countries. They grew and traded all kinds of fruits, but they were a gargantuan monopoly in the banana trading business. El Pulpo’s dominance extended beyond Central America, stretching as far as the West Indies which saw the company control 603,111 acres of land by 1954. Guatemala, Panama, Costa Rica and Honduras were heavily dependent on the export of bananas, which accounted for a major portion of their total exports — hence these countries earned the nickname, banana republics. As a result the company had immense control over the economies of these nations and were notorious for bribing local politicians to get their way, as well as ousting leaders that wouldn’t play ball.

Jacobo Arbenz, a democratically elected president of Guatemala, was made an example of by El Pulpo when the company had him ousted by the U.S. government in 1954 for expropriating some of the company’s land and redistributing it. The seeds for instability were sown in the Central American nation which eventually culminated in a 36 year long civil war between 1960 and 1996. El Pulpo left behind a legacy of destruction and death, not just in Guatemala but throughout Central America.

The United Fruit Company became the embodiment of neocolonialism in the region largely due to the influence of the U.S. government and the power of the almighty dollar. While El Salvador wasn’t a direct victim of El Pulpo, just like its Central American neighbors it was not immune to U.S. intervention in the region, mostly evident during the 12 year Salvadoran Civil War that left 75,000 people dead, the majority of which were civilians. Today El Salvador faces a different version of El Pulpo in the form of the global fiat financial system represented by the IMF.

On September 7 2021 El Salvador made history by becoming the first country in the world to officially adopt Bitcoin as legal tender. Almost immediately the IMF and the World Bank were quick to issue stern warnings to El Salavador’s government about this policy decision, urging them to reverse it. After all they are “guardians of the international financial system,” like Agent Smith in the movie The Matrix. What started out as an experiment in El Zonte (popularly known as Bitcoin beach) in 2019, thanks to an anonymous donor and the tireless efforts of surfer Michael Peterson, has now morphed into a revolutionary movement that inspired Bitcoin City, Bitcoin-backed bonds (aka Volcano Bonds) and financial inclusion for 70% of the population that were previously unbanked. 12 years after Bitcoin came into existence, it is now being used as legal tender in a country. El Salvador may have been the first to adopt Bitcoin, but it definitely won’t be the last.

Just like how the United Fruit Company had Latin America in its grip, the IMF wields a tremendous amount of power over the global economy. Established in 1944 at the Bretton Woods conference, the IMF’s initial role was to secure international monetary cooperation, to ensure stability of currency exchange rates and to expand international liquidity. After President Nixon closed the gold window in 1971, it lost its authority to regulate exchange rates and the IMF pivoted to being a lender of last resort to distressed nations — a mission that has achieved lackluster results to date. For example, a Heritage Foundation study shows that IMF loans to developing countries have been mostly ineffective and some of the countries that received these loans were worse off economically afterwards:

- Of the 89 less developed countries that received IMF loans between 1965 and 1995, 48 are no better off economically today than they were before receiving IMF loans.

- Of these 48 countries, 32 are poorer than they were before receiving IMF loans.

- Of these 32 countries, 14 have economies that are at least 15 percent smaller than when they received their first IMF loans.

With these results in mind let’s turn our attention back to El Salvador to try and figure out why the IMF is vehemently against Bitcoin’s legal tender status. After all, El Salvador is a small country with a population of just ~6.5 million people and a GDP of $25 billion — why then does the IMF perceive Bitcoin adoption by El Salvador as “posing risks to financial stability, financial integrity and consumer protection?” The simple answer is that the IMF is one of the enforcers of the dollar hegemony in the world and the successful adoption of Bitcoin by any nation state poses a significant threat to the “rules-based order.” The U.S. has de facto veto power over all major decisions made by the organization and has the largest voting power of any nation on earth.

As an alternative monetary system Bitcoin was designed to obsolete the role of trusted third parties like central banks and by extension organizations like the IMF. Given the fact that El Salvador is a dollarized economy, the circulation of a U.S, dollar alternative like Bitcoin, may eventually reduce the role of the dollar in transacting, not just in El Salvador but throughout Central America and the rest of the global south. This would slowly usher in a multi-polar world and could possibly lead to bitcoin replacing the dollar as the global reserve currency. In such a world, there is absolutely no need for organizations like the IMF.

The bitcoin-backed bonds have also ruffled the feathers of the IMF with some directors “expressing concern over the risks associated with issuing bitcoin-backed bonds.” The brainchild of Samson Mow, the $1 billion of Volcano Bonds will be used to buy $500 million worth of Bitcoin and $500 million will go towards infrastructure, including infrastructure to harness volcanic energy to mine bitcoin. The global bond market is worth $100 trillion and a successful bond issue will not only be transformative for the market but will serve as a proof of concept for other countries seeking an exit out of the IMF’s system of fiat-based ponzi scheme debts. This is a perspective that prominent investor Simon Dixon echoed in a recent interview where he said,

“If [El Salvador] succeeds, this is a big problem for the business model of the IMF. They’re not a bailout company, they’re not a mechanism for developing the world…They’re a mechanism for dollarizing the world and implementing a global central bank digital currency on top of their special drawing rights, so they can maintain control of their mechanisms.”

As the modern day El Pulpo, the IMF is hell bent on maintaining their dominant position in the global economy and despite all the positive developments that could accrue to El Salvador thanks to the Bitcoin Law, they will continue to vehemently oppose it. They will use every tool at their disposal to not only ensure the reversal of Bitcoin’s legal tender status in El Salvador but to stop other fiat-enslaved countries from following a similar path to debt freedom. A recent example of this would be the $45 billion bailout package they approved for Argentina in March which included a provision that forces the Argentinian government to crack down on cryptocurrencies and discourage their use as a condition for the bailout. The clause detailed Argentina’s efforts “to discourage the use of cryptocurrencies with a view to preventing money laundering, informality, and disintermediation” in order to “to further safeguard financial stability.” Argentina’s central bank subsequently banned financial institutions in the country from offering any Bitcoin or cryptocurrency related services to their clients. This is just the beginning and it wouldn’t be surprising to see this clause being included in every bailout package going forward.

With the Bitcoin price at ~$20,000 as of time of writing, approximately 56% lower than it was during El Salvador’s adoption last year, mainstream media pundits are quick to point out El Salvador’s paper losses, which are estimated to be anywhere between $40 million and $60 million on the Bitcoin that the government bought, as evidence of the dismal failure of the “Bitcoin policy.” This analysis is misleading in that it equates a drop in portfolio value to actual realized losses, which aren’t applicable in this case as El Salvador hasn’t sold a single bitcoin. Secondly it’s also myopic because by exchanging dollars with an infinite supply, for bitcoin, a scarce digital bearer-asset, President Bukele’s move insured El Salvador against dollar debasement. Interestingly enough prior to the Bitcoin Law, El Salvador was hardly mentioned in the Western mainstream media except in relation to gang violence. However, ever since the Bitcoin Law came into effect, President Nayib Bukele has been accused of gambling the country’s resources on bitcoin, with the policy being deemed a failure.

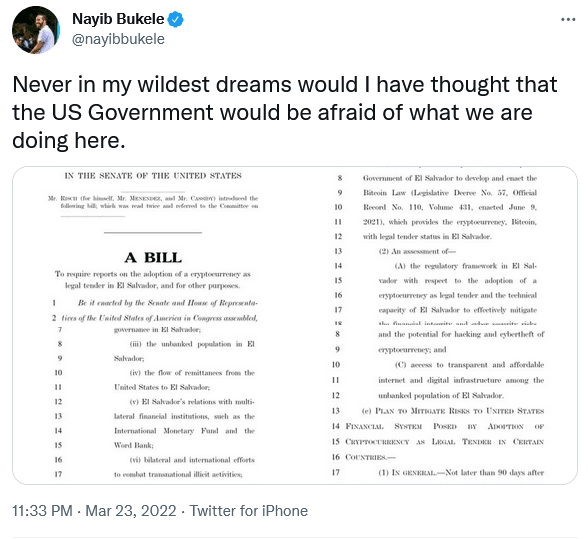

Furthermore, El Salvador’s sovereign debt rating has been downgraded by Fitch, Moody’s and S&P to junk status, with all three rating agencies citing the sovereign’s adoption of Bitcoin as a threat to securing IMF financial support as one of the reasons for the downgrade. According to S&P “The risks associated with the adoption of bitcoin as legal tender in El Salvador seem to outweigh its potential benefits. There are immediate negative implications for the credit.” On February 16, U.S. Senators, James Risch (R-Idaho), Bob Menendez (D-N.J.) and Bill Cassidy (R-La.) introduced the “Accountability for Cryptocurrency in El Salvador (ACES) Act,” which is legislation that compels the State Department to write a report on El Salvador’s adoption of Bitcoin as legal tender and a plan of action to mitigate risks arising from this. To put “risks” in perspective, El Salvador’s GDP ($25 billion) is 840 times smaller than the U.S.’s GDP ($21 trillion). Commenting on the bill in a press release Dr. Cassidy said, “El Salvador recognizing Bitcoin as official currency opens the door for money laundering cartels and undermines U.S. interests … If the United States wishes to combat money laundering and preserve the role of the dollar as a reserve currency of the world, we must tackle this issue head on.” It’s undeniable that this is a tactic straight out of El Pulpo’s playbook whose intention is to stymie El Salvador’s Bitcoin adoption.

Despite all the challenges and attacks there is a silver lining in the clouds. From the time the Bitcoin Law came into effect a year ago El Salvador has seen a 30% increase in tourism according to Salvadoran Tourism Minister, Morena Valdez. This year alone El Salvador has welcomed 2.2 million tourists and in a recent tweet President Bukele noted that tourism in the country had recovered to pre-pandemic levels, citing “Bitcoin and surf” coupled with the ongoing crackdown on gangs, as the major reasons for the recovery. In addition to this, the beach town of El Zonte is set to receive over $200 million worth of infrastructure upgrades. Given the uptick of tourism due to El Zonte’s iconic status from Bitcoin Beach, the money is being used to finance the construction of brand new amenities to cater to the tourists flocking to the town. With tourism currently contributing 9.3% to El Salvador’s overall GDP these are all very significant positive developments.

El Salvador’s GDP grew by 10.3% in 2021 and it’s worth noting that prior to 2021 El Salvador had never had double digit GDP growth. Exports for 2021 also grew by an additional 13%. Annual remittances to El Salvador account for 24% of its GDP (approximately $6 billion) with 70% of Salvadorans reliant on them for survival. Thanks to Bitcoin they could save at least $400 million in money transfer fees annually which equates to 1.5% of El Salvador’s GDP. Furthermore since there are now more Salvadorans with Bitcoin wallets than those with bank accounts these cost savings are immediately being realized by the majority of the populace. The media conveniently ignores mentioning these and numerous other immediate benefits that have materialized post Bitcoin adoption.

In 1958 Guinea attempted to claim its monetary sovereignty from the French by leaving the CFA franc zone. Over a 2 month period the French pulled out of Guinea taking everything with them from light bulbs to sewage pipe plans, and they even went as far as burning essential medicines. The next step was to destabilize Guinea and undermine any efforts of economic prosperity through a covert operation that became known as “Operation Persil,” where they counterfeited Guinean bank notes and flooded them into the country. The intention of the operation was to engineer economic collapse via hyperinflation. The French produced banknotes that proved to be more resistant to the humidity of the Guinean climate better than the official bank notes, thus economic instability in the country was successfully triggered and the Guinean economy collapsed. For the El Pulpos of the world like the IMF, destroying Bitcoin is an absolute necessity because failure to do so would lead to their extinction. It would be naive to assume that these organizations will let El Salvador walk out of their fiat ponzi-scheme system without putting up a fight.

As the cracks in the fiat monetary system begin to appear, Bitcoin is a defense system against financial censorship, dollar debasement and seizure like in the case of the confiscation of Russia’s foreign reserve; it still achieves global consensus in an adversarial environment. Bitcoin is a tool for resisting all forms of monetary repression and El Salvador’s adoption of it is a declaration of monetary independence from the dollar imperialism that grips the world. As geopolitical tensions rise and the gradual de-dollarization of the world occurs, the options for nation states will be a dollar standard vs a BRICS standard or a Bitcoin standard. Having chosen the latter, El Salvador is the new Camelot.

This is a guest post by Kudzai Kutukwa. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc. or Bitcoin Magazine.

Comments (No)